Jumbo Loan Requirements Florida 2026: Qualifying for SWFL Luxury Homes

- Team 239

- May 2

- 12 min read

The $832,750 threshold in Florida isn't just a regulatory limit; it's the new baseline for luxury entry in 2026. While the Naples median sale price settled at $587,500 in March 2026, the most sought-after estates in Marco Island and Bonita Springs require a more sophisticated financing strategy. Mastering the jumbo loan requirements Florida 2026 is the essential first step to navigating a market where liquidity is the ultimate currency. We know that facing a strict 43% debt-to-income ratio or the complex documentation required for self-employed buyers can feel like a hurdle to your lifestyle goals.

You probably realize that modern lending now prioritizes "liquidity-backed" trust over simple credit scores. This article promises to give you total clarity on the 2026 criteria so you can start your luxury home search with a competitive edge. We'll provide a precise qualification checklist, explain the impact of the $832,750+ limit, and show you why having 6 to 12 months of post-closing cash reserves is the standard for securing the best rates in Southwest Florida today.

Key Takeaways

Learn why the 2026 conforming limit of $832,750 redefines the luxury entry point for Florida's high-velocity real estate markets.

Discover the updated jumbo loan requirements Florida 2026, including why a 720 credit score is the new baseline for securing competitive interest rates.

Understand the "liquidity-backed" trust model, where 20% down payments and 12 months of cash reserves are standard for Southwest Florida buyers.

Navigate the unique financing nuances of gated communities and new construction homes in Naples, Marco Island, and Bonita Springs.

Prepare for the luxury search by securing a mandatory pre-approval, the essential credential for accessing exclusive SWFL property showings.

Table of Contents What is a Jumbo Loan in Florida for 2026? Core Financial Requirements for a Florida Jumbo Mortgage Down Payments and Post-Closing Cash Reserves Jumbo Loans for Naples and Estero Luxury Properties Next Steps: Securing Your 2026 Jumbo Loan with Team239

What is a Jumbo Loan in Florida for 2026?

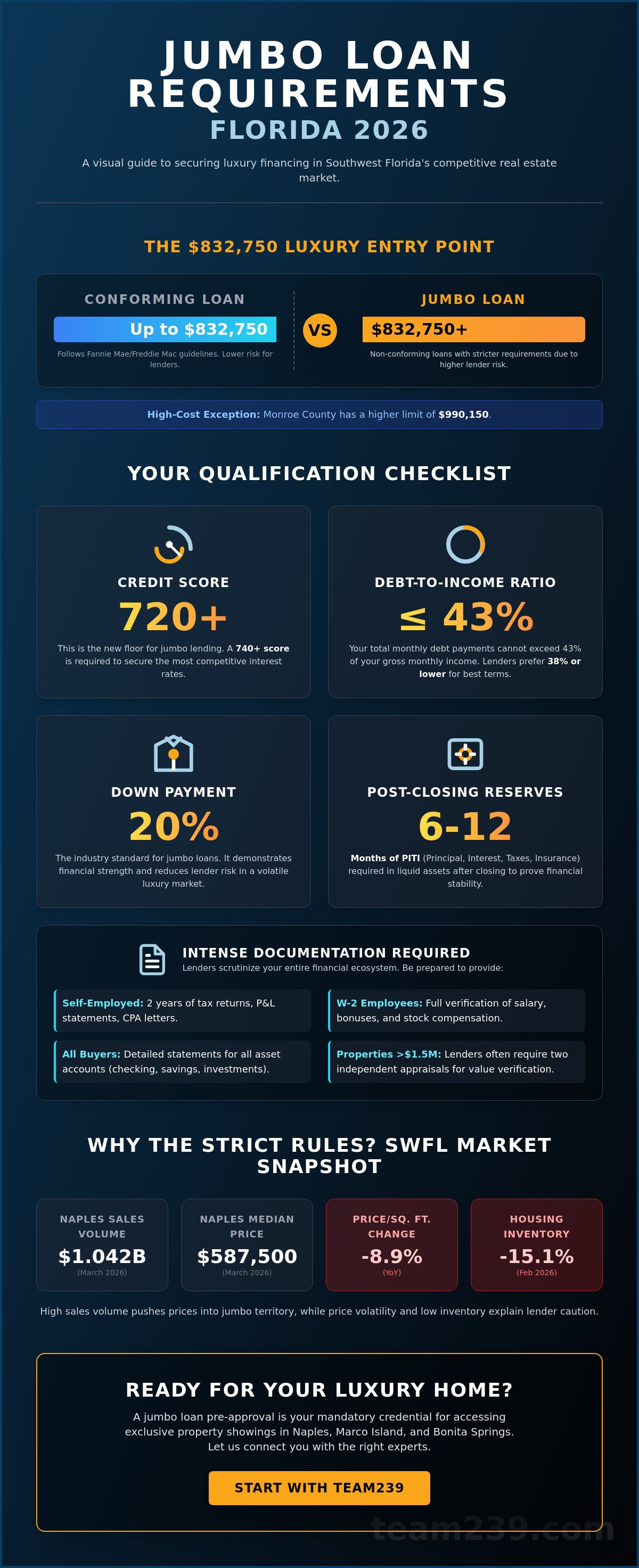

In the Florida real estate market, the line between a standard mortgage and a luxury financing vehicle is drawn at exactly $832,750. This figure represents the 2026 baseline conforming loan limit. If your loan amount exceeds this number, you're entering the territory of a jumbo mortgage. Understanding what a jumbo mortgage is helps clarify why these loans come with a different set of rules. While a standard loan follows guidelines set by Fannie Mae or Freddie Mac, a jumbo loan is "non-conforming." This means lenders can't sell these loans to the government. They keep the risk on their own books or sell to private investors. It's a higher-stakes game for everyone involved.

The FHFA adjusted the 2026 limits to $832,750 to reflect the price appreciation Florida saw throughout 2025. In most of Southwest Florida, including Collier and Lee counties, this is your hard ceiling. However, Monroe County remains a high-cost exception with a limit of $990,150 for single-unit properties. For buyers in Naples or Marco Island, the jumbo loan requirements Florida 2026 are often the only path to a home. With March 2026 sales volume in Naples hitting $1.042 billion, it's clear that luxury properties aren't just a niche. They're the engine of the local market. Even as overall housing inventory decreased by 15.1% in February 2026, prices stayed high enough to push most single-family buyers into the jumbo category.

The 2026 Conforming Limit vs. Jumbo Threshold

Visualizing the $832,750 line is simple: anything above it requires non-conforming financing. This limit is calculated based on year-over-year home value changes across the state. In Naples, where sales activity remains robust despite price adjustments, many single-family homes naturally exceed this threshold. If you're looking for a home in a gated community or a waterfront estate, you're almost certainly dealing with a jumbo loan.

Why Lenders View Jumbo Loans as Higher Risk

Lenders treat these loans with extra caution because they lack GSE backing. This lack of protection leads to much tighter jumbo loan requirements Florida 2026. Lenders also worry about luxury market volatility. In March 2026, the median price per square foot in Naples dropped 8.9% year-over-year. To compensate for this appraisal risk, banks demand deeper documentation and higher liquidity from every luxury buyer. They aren't just looking at your income; they're looking at your entire financial ecosystem to ensure long-term affordability.

Core Financial Requirements for a Florida Jumbo Mortgage

Qualifying for luxury financing in Southwest Florida has become a game of precision. While standard loans follow the conventional conforming loan limits of $832,750, jumbo lenders in 2026 operate with a much thinner margin for error. They're looking for a specific financial profile that proves you can handle the weight of a multi-million dollar asset. This isn't just about having a high income. It's about demonstrating a holistic financial strategy that remains resilient even if the market shifts. For most jumbo loan requirements Florida 2026, the scrutiny begins with your credit history and ends with your specific property type.

The documentation process is particularly intense for self-employed entrepreneurs. If you're a business owner looking in Naples, expect to provide two years of full tax returns, year-to-date profit and loss statements, and potentially a letter from your CPA. W-2 employees have it slightly easier, but lenders still dig deep into bonus structures and stock-based compensation to ensure income stability. If the property exceeds $1.5 million, don't be surprised if the lender requires two independent appraisals to verify the value. This protects the bank against the 8.9% price-per-square-foot decline Naples saw in early 2026.

The 2026 Credit Score Benchmark

In 2026, a 720 score is effectively the floor for jumbo lending. While some programs might exist for lower scores, they usually come with punitive interest rates. To secure the most competitive 5.875% rates seen in May 2026, you'll want a score of 740 or higher. Every recent credit inquiry matters. If you're planning a luxury purchase, pause all other major credit activity. We often recommend that our clients at Team239 audit their reports six months in advance to fix any errors that could stall a high-value closing.

Navigating the 43% DTI Rule

Your Debt-to-Income (DTI) ratio is the most critical metric for long-term affordability. Most lenders cap the total back-end ratio at 43%, though some prefer a conservative 38% for the best terms. In Florida, your DTI is heavily influenced by 2026 property insurance premiums, which must be factored into your monthly housing expense. Debt-to-Income ratio is the percentage of your gross monthly income that goes toward paying your monthly debt obligations, including your future mortgage, taxes, and insurance. Managing this ratio effectively is the key to proving you aren't over-leveraged in a shifting market.

Down Payments and Post-Closing Cash Reserves

Cash is the ultimate trust builder in luxury lending. While credit scores prove your character, your down payment and reserves prove your capacity. In 2026, the standard for a jumbo mortgage in Florida remains 20% down. Yes, 10% programs exist, but they often come with a "liquidity tax" in the form of higher interest rates or stricter debt-to-income limits. Jumbo loan requirements have evolved to prioritize stability over leverage. If your credit score is slightly below the 740 benchmark, a larger down payment of 25% or 30% can often bridge the gap and convince a lender to approve your application.

Lenders look beyond the down payment to your post-closing world. They want to see that you aren't "house poor" the moment you get the keys. Acceptable assets for these reserves include liquid cash, brokerage accounts, and even a portion of your 401(k) or IRA. Restricted stock units (RSUs) are also increasingly accepted by modern lenders, provided they're fully vested. This holistic view of your wealth is a cornerstone of the jumbo loan requirements Florida 2026, ensuring that luxury buyers have the staying power to weather any economic shift.

Calculating Your Reserve Requirements

The 6-to-12 month rule is non-negotiable for most luxury programs in 2026. This means you must have enough liquid assets to cover your entire PITI (Principal, Interest, Taxes, and Insurance) for up to a full year. Lenders check for "seasoning," meaning these funds must have been in your account for at least 60 to 90 days. Large, unexplained deposits right before closing will trigger red flags. It's better to move your funds into the correct accounts well before you start making offers on Gulf-front properties.

Down Payment Strategies for SWFL Luxury Buyers

Strategic buyers often use the "80-10-10" approach to manage cash flow. This involves an 80% first mortgage, a 10% second mortgage, and a 10% cash down payment. It's a clever way to keep your primary loan closer to conforming limits while still securing high-value luxury homes for sale in Naples FL. In a high-interest 2026 environment, putting 30% down isn't just about qualification. It's a defensive play to reduce monthly carry costs. Every dollar of equity you build at closing is a hedge against future market volatility.

Jumbo Loans for Naples and Estero Luxury Properties

Financing a home in Southwest Florida requires more than just a high credit score; it requires a deep understanding of how local property types interact with lender guidelines. In Naples and Marco Island, resort-style living is the standard. However, lenders apply specific scrutiny to gated communities and high-rise condominiums. The "Condo-Jumbo" challenge is particularly relevant on Marco Island. Following the 2026 implementation of new structural integrity regulations, lenders now require exhaustive reserve studies before approving non-conforming loans for high-rise units. If the association's financials don't meet the jumbo loan requirements Florida 2026, your financing could stall regardless of your personal wealth.

Estero presents a different set of variables. With the median sale price in Estero dropping 20.6% year-over-year as of February 2026, appraisals have become the ultimate gatekeeper. Lenders are increasingly sensitive to these "market resets." They often look for more recent comparable sales within a tighter two-mile radius to justify the loan-to-value ratio. This local volatility means your financing strategy must be agile. You need a team that understands why a price adjustment in one neighborhood doesn't necessarily devalue a luxury estate three miles away.

Financing New Construction in SWFL

The new construction homes Bonita Springs market offers incredible opportunities for custom builds, but the financing is complex. Construction-to-permanent jumbo loans are the preferred vehicle here. These loans allow you to lock in your interest rate during the build phase, which is critical given that high-end projects in Naples can take 12 to 18 months to complete. Working with a local expert like Team239 ensures your lender understands the specific nuances of SWFL developers and community timelines.

The Impact of HOA and CDD Fees on Qualification

In Naples, luxury HOA fees can easily exceed $1,000 per month. These aren't just "extra costs"; they're direct hits to your debt-to-income ratio. Lenders treat these fees exactly like a car payment or credit card debt. Newer developments in Estero also frequently include Community Development District (CDD) fees. These are often folded into your property tax bill, but lenders separate them to assess your true monthly carry. Budgeting for these "hidden" costs early in the process is the only way to ensure your DTI remains within the 43% ceiling. If you're ready to see how these factors impact your buying power, contact the Team239 experts for a strategic consultation.

Next Steps: Securing Your 2026 Jumbo Loan with Team239

Securing a luxury estate in Southwest Florida isn't just a financial transaction; it's a strategic operation. In the high-stakes markets of Naples and Marco Island, a simple pre-qualification letter carries very little weight. To meet the jumbo loan requirements Florida 2026, you need a fully underwritten pre-approval before you even request a showing. Sellers of multi-million dollar properties expect proof that your liquidity and credit have already been vetted by a professional. This level of preparation signals that you're a serious buyer in a market where closed sales volume reached $1.042 billion in March 2026. Without it, you risk losing your dream home to a more prepared competitor.

Your "Jumbo Folder" should be ready before you start touring homes. Lenders in 2026 are meticulous, requiring a clear digital trail of your financial health. Start by gathering these essentials to streamline the process:

Two years of full personal and business tax returns.

Year-to-date Profit and Loss statements for self-employed entrepreneurs.

The last 90 days of bank and brokerage account statements.

Verification of post-closing reserves covering 6 to 12 months of mortgage payments.

Documented proof of any large deposits or vested stock options.

Having these documents ready allows us to move with the velocity required to win. We act as your strategic partner, coordinating with "jumbo-friendly" lenders and specialized appraisers who understand the nuances of the Southwest Florida luxury market. This collaborative approach ensures that your financing strategy is as sophisticated as the home you're buying.

The Pre-Approval Advantage in a Competitive Market

There's a massive difference between a lender's quick estimate and a true jumbo pre-approval. A fully underwritten approval means a human underwriter has already reviewed your "Jumbo Folder" and cleared your file for a specific loan amount. This turns your offer into a "cash-like" proposition. In Naples, where active inventory decreased 18.3% year-over-year in March 2026, being the most prepared buyer in the room is your biggest advantage. We leverage our deep local relationships to ensure your offer stands out to sellers who value certainty over speculation.

Your 2026 SWFL Home Search Starts Here

Integrating your financing strategy with our Naples Florida homes for sale guide is the smartest way to begin. Kristin and Jonathan Van Heukelom don't just find you a house; we manage the entire luxury ecosystem. We guide you through the jumbo loan requirements Florida 2026 and ensure every detail, from the structural integrity of a condo to the CDD fees in Estero, is factored into your plan. Contact Team239 today to begin your luxury home journey and let's secure your piece of the Florida dream together.

Master the 2026 Luxury Market Today

Navigating the high-end landscape of Southwest Florida requires a blend of financial precision and local market intelligence. By mastering the jumbo loan requirements Florida 2026, you've moved past the initial hurdles of debt-to-income caps and reserve requirements. This clarity allows you to focus on what truly matters: selecting the right estate in Naples, Bonita Springs, or Marco Island. In this tier of real estate, your financing strategy acts as your strongest credential, opening doors to the region's most exclusive properties.

Team239 brings over 10 years of SWFL luxury market expertise to your corner. Led by local experts Kristin and Jonathan Van Heukelom, we specialize in the unique demands of new construction and resort communities. We don't just facilitate sales; we act as strategic advisors who ensure your financing and lifestyle goals align perfectly. Ready to find your Naples luxury home? Browse our exclusive listings today. With the right team and a solid plan, your transition to the Florida luxury lifestyle will be seamless and rewarding.

Frequently Asked Questions

What is the jumbo loan limit in Florida for 2026?

The jumbo loan limit for most Florida counties in 2026 is any loan amount exceeding $832,750. This baseline was set by the FHFA to reflect the home value appreciation seen across the state throughout 2025. Monroe County remains a high-cost exception with a significantly higher limit of $990,150 for single-unit properties.

Can I get a jumbo loan with a 10% down payment in Naples?

Yes, you can secure a jumbo loan with a 10% down payment in Naples, though it often triggers more rigorous jumbo loan requirements Florida 2026. While 10% is possible for highly qualified buyers, a 20% down payment remains the industry standard for Southwest Florida luxury homes. Putting less than 20% down usually results in stricter debt-to-income caps or higher interest rates.

What credit score is needed for a jumbo loan in Florida in 2026?

Lenders typically require a minimum FICO score of 680 to 700 to qualify for a jumbo mortgage in 2026. To access the most competitive market rates, you'll likely need a score of 740 or higher. Maintaining a clean credit profile without new major inquiries is essential during the six months leading up to your luxury home purchase.

Are jumbo loan rates higher than conforming rates in 2026?

As of May 1, 2026, jumbo loan rates in Florida are actually lower than national conforming averages, sitting at approximately 5.875%. This compares favorably to national conforming rates that ranged between 6.53% and 6.66% during the same period. These competitive rates make jumbo financing a strategic choice for buyers in the Naples and Estero markets.

How many months of cash reserves do I need for a $1 million mortgage?

Most lenders require you to demonstrate 6 to 12 months of post-closing cash reserves for a $1 million mortgage. These reserves must cover the full monthly PITI payment, which includes principal, interest, taxes, and insurance. You can meet this requirement using liquid assets in checking and savings accounts or vested balances in retirement and brokerage accounts.

Do jumbo loans require two appraisals in Florida?

Yes, many lenders require two independent appraisals for any Florida property with a purchase price exceeding $1.5 million. This policy protects the lender against market volatility, such as the 8.9% decline in Naples' price per square foot recorded in March 2026. Having two valuations ensures the loan-to-value ratio is based on a conservative and accurate market assessment.

Can I use a jumbo loan to buy a condo in Marco Island?

You can use a jumbo loan for a Marco Island condo, but the building must pass a rigorous structural integrity and reserve study. Following new 2026 regulations, lenders won't approve non-conforming loans for units in buildings with insufficient maintenance reserves. This rebound in buyer confidence has led to a surge in condo sales for associations that meet these strict transparency standards.

What documents do I need to apply for a jumbo loan in 2026?

To apply, you'll need two years of tax returns, 90 days of bank statements, and proof of all post-closing reserves. Self-employed buyers must also provide year-to-date profit and loss statements. Under Florida bill CS/HB 381, which takes effect July 1, 2026, your lender is required to follow enhanced security protocols to protect the sensitive data contained in these documents.

Comments