Mortgage Pre-Approval for Luxury Homes in Naples: The 2026 Strategic Guide

- Team 239

- Jun 1

- 13 min read

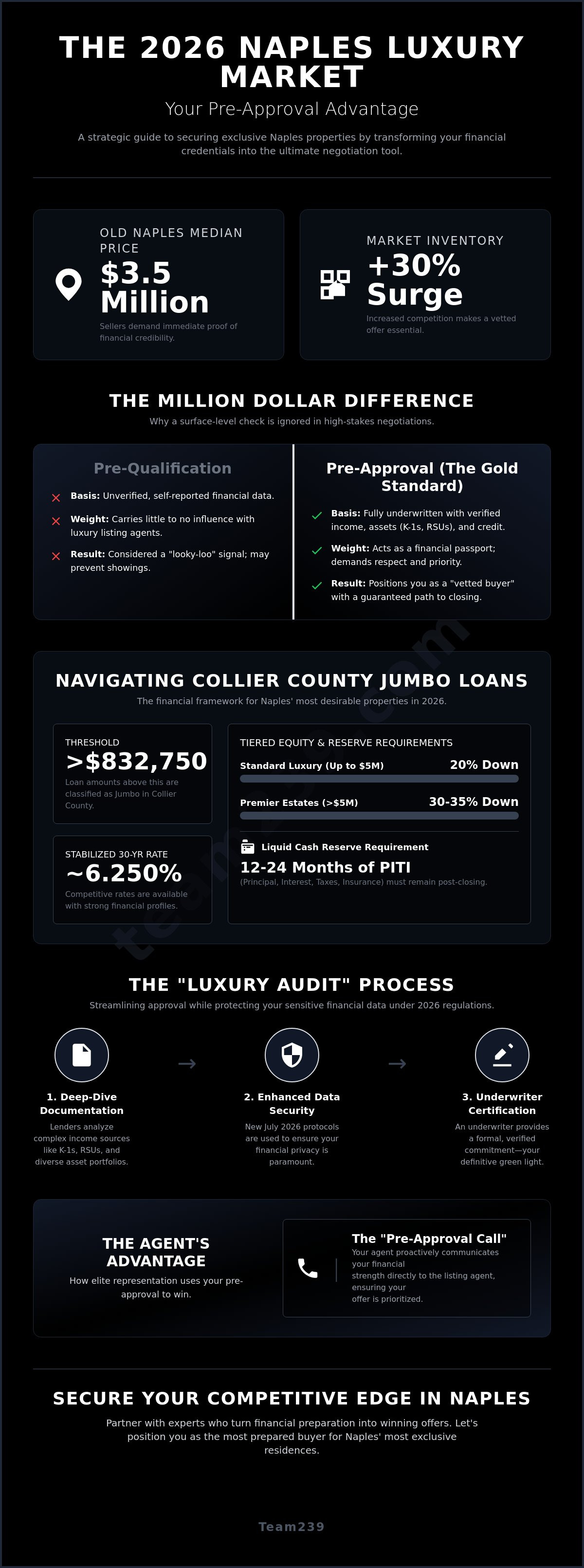

In the 2026 Naples market, a mortgage pre-approval is not a sign of debt; it's a strategic credential that functions as your private key to the city's most exclusive estates. You likely understand that in a landscape where the median price in Old Naples has reached $3.5 million, sellers expect more than just interest. They demand immediate proof of credibility. Securing a mortgage pre-approval for luxury homes in Naples can feel intrusive when dealing with complex K-1 structures or RSU-heavy portfolios, especially with the heightened documentation standards Florida lenders now require.

You deserve a process that respects your privacy while positioning you as the most prepared buyer in the room. This guide empowers you to master the financial strategies required to secure an exclusive residence with total confidence. We will explore how to navigate current 6.250% Jumbo loan rates, utilize new July 2026 data security protocols, and turn your complex income structure into a decisive competitive advantage during negotiations.

Key Takeaways

Learn why a verified lender commitment acts as a strategic privacy shield and the ultimate negotiation tool in the competitive 2026 Naples market.

Discover how to navigate the current Collier County Jumbo loan limits and leverage asset-based lending programs designed for self-employed high-net-worth individuals.

Understand the critical differences between a Proof of Funds and a mortgage pre-approval for luxury homes in Naples to determine which asset best strengthens your offer.

Master the "Luxury Audit" documentation process to streamline your approval while ensuring your sensitive financial data remains secure under new 2026 regulations.

See how elite representation uses the "Pre-Approval Call" to proactively communicate your financial strength directly to listing agents in neighborhoods like Port Royal.

Table of Contents

Why Pre-Approval is the Ultimate Negotiation Tool in Naples Luxury Real Estate

Think of a mortgage pre-approval for luxury homes in Naples as your financial passport. It isn't just a preliminary credit check; it's a formal, verified commitment from a lender that you've been fully underwritten. In a market where inventory has surged by 30%, sellers have become increasingly selective about who they allow through their front doors. They demand immediate proof of credibility before disclosing floor plans or private security details. Obtaining a mortgage loan in this price bracket requires a strategic approach that turns your financial profile into a position of strength.

A pre-approval sets the ceiling for your negotiation strategy long before you step onto a property. It defines your boundaries and gives you the confidence to act decisively when the right opportunity appears. When you present an offer backed by a verified commitment, you aren't just another interested party. You're a "vetted" buyer who represents a guaranteed path to closing. This psychological edge is vital in 2026, as sellers prioritize certainty and speed over slightly higher but uncertain bids.

The "Vetting" Culture of Naples Gated Communities

In exclusive enclaves like Port Royal or Grey Oaks, privacy is the primary currency. Listing agents in these neighborhoods act as professional gatekeepers. They use pre-approval to filter out "looky-loos" who lack the capital for the $3.5 million median entry point seen in Old Naples. Without this document, your request for a private showing may be denied to protect the seller's security and time. For a deeper look at these specific neighborhoods and their entry requirements, consult our Luxury Homes for Sale in Naples FL: The 2026 Insider’s Guide.

Pre-Qualification vs. Pre-Approval: The Million Dollar Difference

Pre-qualification is a surface-level estimate that's often ignored by top-tier listing agents. It relies on unverified data and carries little weight in high-stakes deals. A true mortgage pre-approval for luxury homes in Naples involves a "Luxury Audit," which requires a deep dive into your K-1s, liquid assets, and complex income streams. Sellers in 2026 expect a document that proves a lender has already done the heavy lifting of verification. The 2026 gold standard for a pre-approval letter is an underwriter-certified document that confirms both asset liquidity and income stability, providing a definitive financial green light to sellers.

By securing this credential early, you bypass the friction that often stalls luxury transactions. You move from being a prospect to a partner in the deal, ensuring that when you find the perfect Naples residence, your financial readiness is never in question.

Navigating Jumbo Loans and Portfolio Lending in the 2026 Market

In 2026, the financial boundary for luxury real estate in Collier County is precisely defined. Any loan amount exceeding $832,750 is classified as a jumbo mortgage, moving you beyond the reach of standard conforming guidelines. While the 30-year jumbo mortgage rate has stabilized around 6.250%, the complexity of these loans requires more than just a high credit score. Securing a mortgage pre-approval for luxury homes in Naples now hinges on your ability to navigate tiered down payment structures and rigorous liquidity requirements that national lenders often struggle to process efficiently.

Local Florida lenders frequently outperform national institutions in this space because they understand the nuances of the Naples market, from specific HOA assessments to coastal insurance requirements. They treat the mortgage pre-approval process as a bespoke financial strategy rather than a box-ticking exercise. This localized expertise ensures that your financing doesn't hit a bottleneck during the critical final days of a high-stakes transaction.

Jumbo Loan Nuances for High-Value Properties

Financing a $2 million residence differs significantly from a $10 million estate in Port Royal. While a 20% down payment is standard for entry-level luxury, homes exceeding the $5 million mark often require 30% to 35% equity. Beyond the down payment, "Reserve Requirements" have become a focal point in 2026. Lenders typically expect to see 12 to 24 months of liquid cash reserves (PITI) remaining in your accounts after closing. If you are purchasing a secondary home or an investment property, expect these requirements to tighten, often with a slight premium on the interest rate to account for the increased risk profile.

Portfolio Lending for Complex Financial Profiles

Standard debt-to-income (DTI) ratios often fail to capture the reality of high-net-worth individuals. If your wealth is tied up in RSUs, stock options, or complex K-1 income from multiple entities, portfolio lending is your most effective path. These "Asset-Based Lending" programs allow you to qualify based on your total managed assets rather than just traditional monthly cash flow. Relationship banking plays a massive role here; lenders you already have a history with are more likely to offer flexible terms and competitive DTI caps. When you are ready to align your financial strategy with a specific property, working with a specialized buyer representative ensures your lender and agent are moving in perfect lockstep.

This shift toward asset-depletion models and relationship-based underwriting is the hallmark of the 2026 luxury market. It provides the agility needed to compete with cash offers while maintaining the tax advantages of strategic leverage.

Pre-Approval vs. Proof of Funds: Which One Wins in Port Royal?

In the ultra-high-net-worth enclaves of Port Royal, the question isn't just whether you can afford the property. It's about how you choose to structure the exit from your capital. Sellers in this tier are sophisticated; they understand that a buyer with $50 million in liquidity might still prefer to finance a $15 million purchase to maintain market position. This creates a unique dynamic between the Proof of Funds (POF) and a mortgage pre-approval for luxury homes in Naples. While a POF proves you have the cash, a pre-approval proves you have a lender ready to back your strategy. In 2026, the most successful offers often use both documents to create a "Hybrid Offer" that provides the seller with absolute closing certainty.

The 2026 Naples luxury landscape has shifted. With inventory up by 30% compared to last year, sellers are more flexible, but they remain fiercely protective of their time. A bank-verified POF is often required just to schedule a showing in Port Royal. However, the mortgage pre-approval for luxury homes in Naples is what wins the negotiation. It signals that you've already cleared the rigorous "Luxury Audit" mentioned earlier, removing the financing hurdle from the timeline. This dual-layered approach allows you to compete with all-cash bids by offering the same level of speed and reliability.

The Strategy of Leverage for HNWIs

Why would a buyer with ample liquidity seek financing? In 2026, the decision is often driven by opportunity cost and tax efficiency. If your diversified portfolio is outperforming the 6.250% jumbo mortgage rate, liquidating assets to buy real estate represents a net loss. Savvy investors use leverage to keep their capital working in high-growth sectors while securing a primary or secondary residence. To understand how these financial moves fit into the broader local market, see our Naples Florida Homes for Sale: The Complete 2026 Buyer's Guide.

Protecting Privacy During the Proof of Funds Process

Privacy is a major pain point for luxury buyers. You shouldn't have to expose your entire net worth to a listing agent just to prove you're qualified. We often recommend using a "Bank Letter" as a middle ground. This is a formal statement on bank letterhead confirming you have "funds in excess of the purchase price" without disclosing your exact balance or account numbers. As your representatives, we handle these sensitive documents with extreme discretion, ensuring that only the necessary proof of credibility is shared to protect your financial footprint.

Choosing between cash and financing isn't an either-or scenario. It's a tactical decision that balances liquidity, privacy, and negotiation leverage to ensure you win the deal on your own terms.

Step-by-Step: Securing Your Luxury Mortgage Pre-Approval

Securing a mortgage pre-approval for luxury homes in Naples requires a departure from standard retail banking. You need a lender with a dedicated concierge division that understands high-limit underwriting and complex wealth structures. A standard loan officer might stumble over a $5 million portfolio; a luxury specialist expects it. This process begins with an honest assessment of your credit profile. While a 740 score is excellent for most, the "Luxury Tier" often targets 760 or higher to unlock the most aggressive 2026 jumbo rates. If your score is hovering just below this mark, your lender can often suggest rapid rescoring strategies to bridge the gap before you submit your formal application.

Once you've selected your partner, the focus shifts to the "Luxury Audit." This isn't just about showing income; it's about proving the stability and liquidity of your entire financial ecosystem. This level of preparation allows you to move with the speed of a cash buyer when the right property hits the market. In a landscape where inventory is moving quickly, being "pre-underwritten" is the difference between winning a bid and being an afterthought.

The Luxury Documentation Checklist

Standard W-2s won't suffice here. If you are an entrepreneur or high-net-worth investor, your lender will require a comprehensive data package to verify your borrowing power. Prepare to provide:

Tax Returns: Two years of full personal and business filings, including all schedules and attachments.

Entity Documentation: K-1s for any partnership or S-Corp where you hold a significant interest.

Asset Verification: Three months of statements for brokerage accounts, trusts, and liquid reserves.

Letter of Explanation (LOX): A concise narrative explaining any large recent asset movements or one-time capital gains to the underwriter.

Ask your lender for "TBD Underwriting." This means an actual underwriter reviews your file before you have a property contract. It effectively clears your financial hurdles in advance, allowing you to close in as little as 21 days.

Factoring in Naples-Specific Carrying Costs

Your debt-to-income (DTI) ratio isn't just about your mortgage payment. In 2026, carrying costs in Florida have become a critical variable in the pre-approval equation. Monthly "PITI" calculations must now account for increased wind and flood insurance premiums, which vary based on the home's elevation and construction date. Additionally, many communities in North Naples and Bonita Springs utilize Community Development District (CDD) fees to fund infrastructure. These fees are added to your property taxes and can impact your qualification limit. For a detailed breakdown of how these fees function in specific neighborhoods, explore our New Construction Homes in Bonita Springs, FL: The Complete 2026 Buyer's Guide.

After your letter is finalized, the real work begins. We recommend a strategy call with our team to align your approved budget with current market inventory and neighborhood-specific costs. Connect with Kristin and Jonathan to bridge the gap between your financial approval and your next Naples residence.

Beyond the Paperwork: How Team239 Uses Your Pre-Approval to Win

A mortgage pre-approval for luxury homes in Naples is a static document until it's activated by a strategic negotiation plan. Having the paper is one thing; using it to collapse a seller's resistance is another. Kristin and Jonathan Van Heukelom don't just attach a PDF to an email and hope for the best. We use your financial readiness as a psychological lever to prove that your offer is the most secure path to a successful closing. In a market where inventory has increased, sellers are more anxious about deals falling through. We capitalize on that anxiety by presenting you as a "sure thing."

Our most effective tactic is the "Pre-Approval Call." The moment we submit your offer, we have your lender call the listing agent directly. This isn't a casual chat. Your lender confirms that you've completed the "Luxury Audit," that your complex income structures are already verified, and that the loan is essentially through underwriting. This proactive communication eliminates the listing agent's doubts. It often allows us to negotiate a better price because we're offering the seller a 21-day or 30-day closing certainty that higher, unverified bids can't match.

The Team239 Advantage in Luxury Negotiations

We maintain an elite network of local lenders who meet strict 2026 Southwest Florida standards. We vet these partners to ensure they prioritize the new July 2026 data security protocols, protecting your privacy during every step of the transaction. For our high-profile clients, we act as a "Privacy Barrier," ensuring that sensitive financial details are handled with the discretion required for high-stakes real estate. This methodology consistently wins. In a recent multi-offer situation in Old Naples, our client secured the property despite not being the highest bidder. The seller chose us because our lender's direct confirmation of "TBD Underwriting" status provided a level of confidence the other agents failed to establish.

Ready to Start Your Naples Luxury Journey?

Your path to an exclusive Naples residence starts with a strategy, not a search engine. We provide the local expertise and financial networking required to navigate jumbo lending and portfolio requirements with total transparency. Whether you are looking for a Gulf-front estate or a modern masterpiece in a gated community, your financial positioning will be your greatest asset. Schedule a confidential consultation with our team to align your goals with the city's most prestigious opportunities. Contact Team239 to find your Naples luxury home and turn your 2026 real estate vision into a tangible reality.

Mastering Your 2026 Naples Acquisition

Success in the Southwest Florida luxury market requires more than just interest. It demands a sophisticated financial strategy that prioritizes privacy, leverage, and speed. By securing a mortgage pre-approval for luxury homes in Naples, you transform your offer from a mere proposal into a definitive commitment that commands respect from the city's most elite sellers. You've seen how navigating 2026 jumbo rates and asset-based lending is about more than just numbers; it's about positioning yourself as the most credible buyer in the room.

As a family-led team with over a decade of Southwest Florida expertise, we specialize in representing buyers of waterfront estates and luxury new construction. We provide you with exclusive access to our vetted network of 2026 luxury mortgage partners who understand the complexities of high-net-worth portfolios. Don't leave your next move to chance. Secure your Naples luxury home with Team239 and let us turn your financial readiness into a competitive edge. Your future in Naples is ready for its next chapter, and we're here to ensure it begins with total confidence.

Frequently Asked Questions

Do I need a pre-approval if I am buying a luxury home in Naples with cash?

You don't strictly need a mortgage pre-approval if you aren't financing, but you must provide a bank-verified Proof of Funds (POF) to enter the negotiation. Sellers in high-end communities like Port Royal often require this documentation before they even grant a showing request. Many savvy investors still choose to get a mortgage pre-approval for luxury homes in Naples to keep their financing options open while using their cash position as a secondary safety net.

What is the minimum credit score for a luxury Jumbo loan in 2026?

Most lenders require a minimum score of 700 for jumbo products, but the 2026 "Luxury Tier" standard for competitive rates is 760 or higher. While you can qualify with a lower score, you'll likely face higher interest rates or increased reserve requirements. Lenders today prioritize long-term affordability and stability, so a higher score significantly smoothens the underwriting process for multi-million dollar acquisitions.

How long does a mortgage pre-approval last in the Florida market?

A standard pre-approval is typically valid for 60 to 90 days. Given that Naples inventory has increased by more than 30% recently, your search might take longer than in previous years. It's easy to refresh your status with updated pay stubs or brokerage statements, but you should avoid making large purchases or opening new credit lines during this window to keep your approval active.

Can I get pre-approved for a luxury home if I am self-employed?

Yes, self-employed buyers successfully secure financing every day through portfolio lending and asset-depletion models. Instead of looking at a traditional W-2, lenders will analyze two years of personal and business tax returns along with your K-1 statements. Obtaining a mortgage pre-approval for luxury homes in Naples as an entrepreneur simply requires more front-end documentation to verify the consistency of your cash flow and the health of your business entities.

What are CDD fees and do they affect my mortgage pre-approval?

Community Development District (CDD) fees are infrastructure costs passed on to homeowners through their property tax bills. These fees are included in your total monthly housing expense and directly impact your debt-to-income (DTI) ratio. If you're looking at newer communities in North Naples or Bonita Springs, these costs can be several thousand dollars annually, which might slightly lower your maximum approved loan amount.

Is a local Naples lender better than a national bank for luxury homes?

Local lenders generally offer a significant advantage because they understand Southwest Florida's unique appraisal nuances and insurance requirements. National banks often struggle with the complexity of Naples HOA structures or coastal wind and flood insurance premiums. A local specialist can also make the "Pre-Approval Call" to a listing agent, which provides a level of personal credibility that automated national call centers can't replicate.

How much down payment is required for a $5 million home in Naples?

Expect to provide a down payment of 30% to 35% for properties at the $5 million level. While 20% is common for homes closer to the $832,750 jumbo threshold, higher-tier estates represent more risk to the lender. In addition to the down payment, you'll need to show significant liquid reserves remaining in your accounts after the closing costs are paid to satisfy 2026 liquidity guidelines.

Does a mortgage pre-approval guarantee I will get the loan?

No, a pre-approval is a conditional commitment based on your current financial profile and the property's eventual appraisal. The loan is only guaranteed once the property passes inspection, the title is cleared, and the lender's final "clear to close" is issued. To get as close to a guarantee as possible, ask for "TBD Underwriting," where a human underwriter verifies your entire file before you even sign a purchase contract.

Comments