Understanding Florida Elevation Certificates: A 2026 Guide for SWFL Homeowners

- Team 239

- May 18

- 12 min read

In 2026, an Elevation Certificate is no longer just a boring flood document; it's a high-value asset for property valuation and strategic insurance arbitrage in Southwest Florida. You've likely felt the stress of rising premiums or felt lost trying to decode FEMA's Risk Rating 2.0. It's frustrating when your property feels like a financial moving target due to complex, shifting building codes. Understanding Florida elevation certificates is the most effective way to regain control of your home's narrative and stop the cycle of unexpected insurance spikes.

This guide provides the technical clarity you need to slash unnecessary costs and secure your investment before the 9th Edition of the Florida Building Code takes effect on December 31, 2026. We'll help you master the current FEMA Form FF-206-FY-22-152 to maximize your property's market value and ensure long-term resilience. You'll learn how to leverage precise elevation data for lower premiums, navigate the 50% rule during property improvements, and ensure your next real estate closing is seamless and predictable.

Key Takeaways

Master the technicalities of FEMA-approved documents that verify building height and directly dictate your NFIP insurance rates.

Gain a strategic advantage by understanding Florida elevation certificates to optimize the marketability and value of high-end properties under Risk Rating 2.0.

Identify exactly when an EC is mandatory, from securing a mortgage in a flood zone to managing substantial improvements under the 50% rule.

Streamline your search for existing documents through digital portals and local records to avoid unnecessary surveying costs.

Learn how professional listing services leverage flood risk analysis to ensure your property stands out in the competitive Southwest Florida market.

Table of Contents

What is a Florida Elevation Certificate and Why is it Essential?

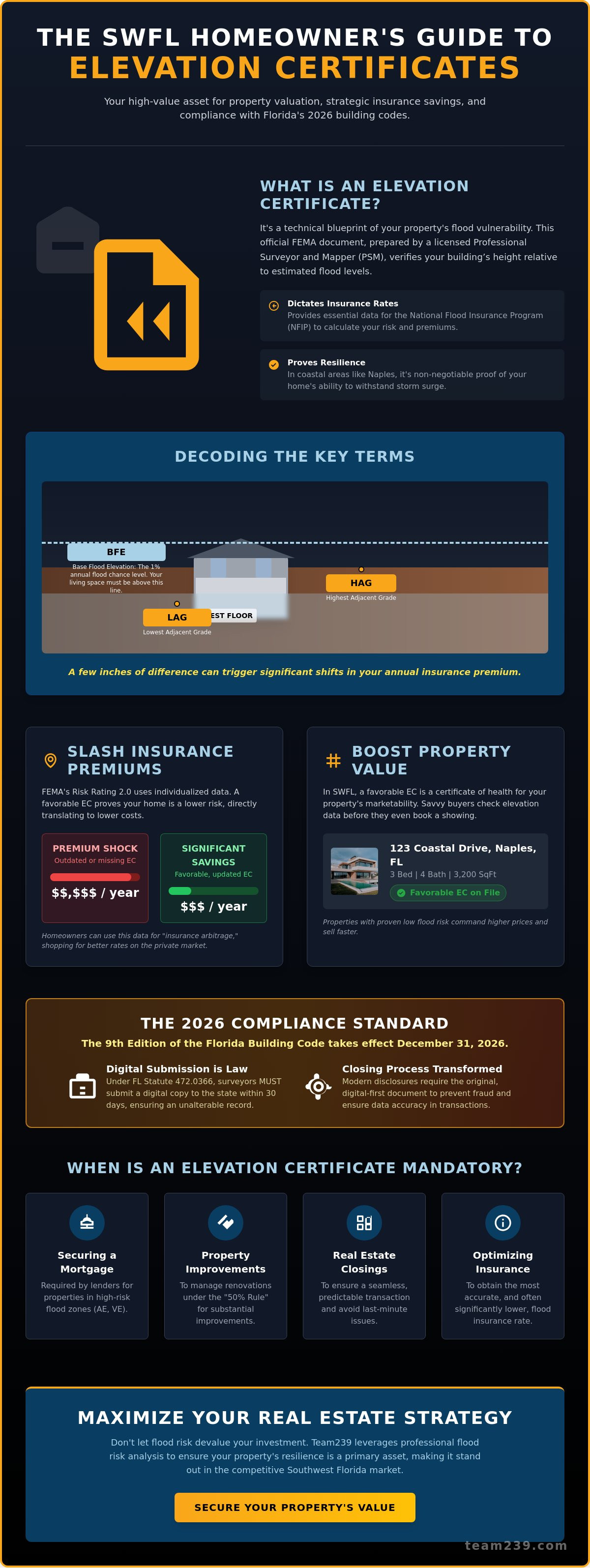

An Elevation Certificate (EC) is a technical blueprint of your property's vulnerability. It isn't just a standard form; it's a FEMA-approved document prepared by a licensed Professional Surveyor and Mapper (PSM) that verifies your building's height relative to estimated flood levels. In Southwest Florida, where water defines our lifestyle and our geography, understanding Florida elevation certificates is the primary step toward financial defense and property protection.

The core purpose of this document is to translate physical geography into insurance data. It provides the essential metrics used by the National Flood Insurance Program (NFIP) to calculate your risk and set your annual premiums. Beyond just compliance, understanding Florida elevation certificates allows you to identify if your property qualifies for lower rates based on its specific construction features. For homeowners in coastal hubs like Naples and Marco Island, the document is non-negotiable. Coastal surge risks make precise elevation data the only way to prove your home's resilience. The relationship between your home’s lowest floor and the Base Flood Elevation (BFE) determines your risk profile. If your floor is below the BFE, your insurance costs will reflect that increased exposure.

Decoding the Key Terms: BFE, LAG, and HAG

Success in SWFL real estate requires a grasp of three critical acronyms. Base Flood Elevation (BFE) represents the water level that has a 1% annual chance of being equaled or exceeded. You want your living space well above this line. The Lowest Adjacent Grade (LAG) and Highest Adjacent Grade (HAG) measure the ground level touching your structure. In Collier and Lee counties, these numbers aren't just trivia; they're the variables in a complex equation that dictates your annual insurance premium. A few inches of difference in the LAG can trigger significant pricing shifts under the current risk-based models.

The 2026 Compliance Standard

The regulatory environment in Florida has shifted toward total transparency and digital precision. Under Florida Statute 472.0366, surveyors must now submit digital copies of every completed Elevation Certificate to the state within 30 days. This shift has been accelerated by the widespread adoption of Forerunner software, which allows local governments to manage and share elevation data with unprecedented speed. When you're involved in a real estate transaction, having an "unaltered" certificate is vital. Modern disclosures require the original, digital-first document to ensure that the data hasn't been tampered with or misinterpreted during the closing process. This digital-first approach ensures that your property's risk profile is accurately reflected in state and federal databases.

How Elevation Certificates Impact Your SWFL Property Value

A property's value in Southwest Florida isn't just about square footage or marble countertops. In 2026, it's increasingly defined by its relationship to the waterline. Understanding Florida elevation certificates is now a critical part of a homeowner's financial strategy. A favorable certificate acts as a certificate of health for your property's marketability. In high-demand areas like Naples, savvy buyers look at the elevation data before they even walk through the front door. They want to know if the home is built to last and if the insurance carry will be manageable.

FEMA's Risk Rating 2.0 fundamentally changed the valuation of high-value homes in Zone VE and Zone AE. Pricing is no longer a broad stroke across a map; it's an individualized risk assessment. If your certificate shows your home is elevated well above the required levels, your property becomes significantly more attractive than a neighbor's home with lower elevations. Conversely, an outdated or missing certificate can lead to "premium shock." This happens when a buyer discovers the actual flood insurance cost is triple what they anticipated; this often leads to stalled negotiations or price drops during the due diligence period.

Insurance Arbitrage for Luxury Homes

Strategic homeowners use elevation data to shop the private insurance market. While the NFIP has strict caps on how much rates can rise annually, private carriers often offer more competitive pricing for homes with superior construction features. Understanding Florida elevation certificates helps you highlight architectural advantages like hydrostatic vents, which allow floodwaters to flow through a foundation rather than pushing against it. A one foot difference in elevation can save thousands in annual premiums, which adds tens of thousands in perceived value to a potential buyer. Highlighting these technical wins makes your home a lower-risk investment compared to the rest of the market.

The "LOMA" Advantage

Sometimes, the map is just wrong. A Letter of Map Amendment (LOMA) is an official document from FEMA that can change a property's flood zone designation. If your elevation certificate proves your ground is naturally higher than the surrounding flood plain, you can apply for a LOMA to move your home out of a high-risk zone. This expands your buyer pool significantly. Many investors won't even look at luxury homes for sale in Naples FL if they require mandatory high-cost flood insurance. Removing that requirement adds instant liquidity and appeal to your asset.

Navigating these technicalities requires a partner who treats real estate as a data-driven investment. Our luxury property listing services integrate this level of flood risk analysis into every marketing strategy to protect your equity and ensure a smooth transaction.

When is an Elevation Certificate Required in Southwest Florida?

An Elevation Certificate isn't just a static record; it's a dynamic requirement triggered by specific financial and regulatory events. In Southwest Florida, the most common trigger is the purchase of a property using a federally backed mortgage within a Special Flood Hazard Area (SFHA). Lenders require this data to ensure the asset is properly protected against potential loss. Beyond the initial purchase, understanding Florida elevation certificates becomes vital when FEMA releases revised Flood Insurance Rate Maps (FIRMs) for Lee or Collier County. If a map revision places your home in a higher-risk zone, a current EC is your primary tool for challenging that designation or securing an accurate rating before premiums escalate.

Transparency is the gold standard in our local luxury market. When you're selling your home, providing a recent EC as part of a comprehensive disclosure package builds immediate trust with sophisticated buyers. It eliminates the guesswork regarding future insurance costs and proves that the property meets modern resilience standards. You'll also find that insurance carriers may request an updated certificate during a policy renewal if they suspect your current data is obsolete or if you're shopping for more competitive rates in the private market.

Navigating the 50% Rule in Naples and Bonita

The "50% Rule" is a critical threshold for homeowners looking to renovate. If the cost of improvements or repairs exceeds 50% of the structure's market value, the entire building must be brought into compliance with current flood elevation requirements. Your EC is the yardstick used by building departments in Naples and Bonita Springs to determine if your floor height allows for these upgrades. This is a major consideration for those looking at new construction homes Bonita Springs, where builders already integrate these requirements into the initial design to protect long-term equity.

Post-Storm Reconstruction Requirements

Recent hurricane seasons taught us that surge events can change the regulatory landscape overnight. If a home sustains "substantial damage," local authorities will require a new certificate to verify that repairs meet the latest Florida Building Code standards. This process ensures that reconstructed homes are better prepared for future events. If you are moving to southwest florida, understanding Florida elevation certificates helps you evaluate whether a property has been properly remediated or if you're inheriting a compliance headache. Always verify that post-storm repairs were backed by a final, digital-only surveyor submission to the state database.

How to Obtain or Find an Elevation Certificate in Florida

Locating an existing record can save you time and money during a real estate transaction. The first step is to search the Florida Division of Emergency Management (FDEM) public portal. Since January 1, 2023, Florida Statute 472.0366 has mandated that surveyors submit a digital copy of every completed certificate to this state database within 30 days. If your home was surveyed recently, it's likely already indexed and waiting for you. If the state portal yields no results, check with the Collier or Lee County building departments. Local municipalities often maintain archives of certificates submitted during the permitting process for new construction or major renovations.

If digital records are missing, your next move is to contact the original builder or the current homeowner. Builders of modern communities in Southwest Florida typically keep copies of the "final" survey on file. When these avenues fail, hiring a licensed Professional Surveyor and Mapper is necessary. Understanding Florida elevation certificates means knowing that only a licensed professional can certify these elevations. Once the survey is complete, ensure your surveyor confirms the digital submission to the state. Finally, review the findings with your insurance agent and real estate advisor to see how the data impacts your premium or property value.

Local Resources for Naples and Marco Island

The City of Naples and the City of Marco Island maintain robust Floodplain Management offices with deep historical records. Marco Island’s "Flood Information" portal is particularly useful for coastal properties where surge data is highly specific. When you're browsing Naples florida homes for sale, starting with a record check is a power move. It reveals if a property is already compliant or if you'll need to factor in the cost of a new survey and potential insurance adjustments before making an offer.

Hiring a Professional Surveyor

Expect a surveyor to take precise measurements of both the interior and exterior of your home. They'll identify the "lowest floor" and compare it against the Base Flood Elevation. While costs for a residential EC in SWFL vary based on property complexity, the investment is small compared to the potential insurance savings. Recent building code adjustments following Hurricanes Ian, Milton, and Helene mean that older certificates might be functionally obsolete. A certificate typically remains valid until the FEMA maps change or the building is physically altered, but in a post-storm environment, a fresh survey ensures your data meets the 2026 standards.

Ready to secure your property's financial future? Contact Team239 today to connect with our network of trusted local surveyors and insurance specialists who specialize in the Southwest Florida coastal market.

Maximizing Your Real Estate Strategy with Team239

Real estate in Southwest Florida is a high-stakes technical game where data is the ultimate currency. At Team239, we don't just list properties; we engineer transactions based on precise risk analysis. Understanding Florida elevation certificates is a cornerstone of our strategy, ensuring that every luxury listing we represent is backed by verifiable data. We integrate flood risk assessments into our workflow from day one, removing the guesswork that often stalls high-value deals. By partnering with a network of the region's most trusted surveyors and insurance specialists, we provide our clients with a clear financial roadmap before they ever reach the closing table.

Transparency regarding elevation isn't just about compliance; it's about speed and security. When buyers see a comprehensive digital record of a home's resilience, they move forward with confidence. This clarity is essential for anyone looking to embrace the southwest florida lifestyle, where the proximity to water is our greatest draw and our most significant variable. Our team ensures that your transition into this market is supported by strategic thinking and technical expertise.

Expert Representation for Sellers

For sellers, a pre-listing EC check is a vital defensive move. We identify potential insurance surprises before your home hits the market, allowing us to address any discrepancies early. By understanding Florida elevation certificates through a marketing lens, we position your elevated home as a premium, low-risk asset. We highlight the tangible financial benefits of your property's height, such as lower annual carry costs and long-term resilience, making it a standout choice for sophisticated investors who prioritize stability.

Due Diligence for Luxury Buyers

Luxury buyers require more than just a home inspection; they need a deep dive into the property's future ownership costs. We analyze elevation certificates during the due diligence period to forecast exactly how FEMA's shifting regulations will impact your bottom line. If a structure is "non-conforming," we explain the long-term implications for future renovations or rebuilds. This level of detail prevents expensive mistakes and ensures your investment is sound. Contact Team239 today for a comprehensive SWFL market analysis that puts data-driven expertise at the center of your search.

Secure Your Southwest Florida Investment

Mastering the technicalities of your property's elevation is the most effective way to avoid insurance spikes and protect your equity. A current certificate is a vital asset for both compliance and marketability in our coastal market. Understanding Florida elevation certificates empowers you to navigate FEMA's Risk Rating 2.0 and the upcoming 2026 building code changes with complete confidence. Whether you're managing a luxury listing in Naples or planning a new construction build in Bonita Springs, these documents are the foundation of a sound real estate strategy.

You don't have to decode these complex regulations alone. Team239 brings over 10 years of local SWFL expertise to every transaction. As specialists in luxury new construction and coastal properties, we're proud to be the MVP Realty Associates top-performing team. We help you turn technical data into a competitive advantage. Contact Team239 for Expert Real Estate Guidance in SWFL and let's ensure your property is positioned for long-term growth and resilience. Your future in paradise is worth the precision.

Frequently Asked Questions

Do I need an elevation certificate if I am paying cash for a Naples home?

You aren't legally required to obtain an elevation certificate for a cash purchase, but skipping it is a significant financial risk. Without this document, you won't have a verified baseline for your flood insurance premiums or a clear understanding of the property's structural vulnerability. Most cash buyers in Naples still insist on a current certificate during the inspection period to ensure they aren't inheriting a high-cost insurance liability.

How long is a Florida elevation certificate valid for insurance purposes?

An elevation certificate doesn't technically expire, but it becomes obsolete if FEMA updates the Flood Insurance Rate Maps (FIRMs) for your area. It also loses its validity if you make structural changes to the home, such as adding an enclosure or changing the foundation. For the most accurate rating in 2026, insurance carriers prefer the current FEMA Form FF-206-FY-22-152 to ensure data matches current standards.

Can I use an old elevation certificate from a previous owner?

You can often use a previous owner's certificate if the building's footprint and the local flood maps haven't changed. However, understanding Florida elevation certificates involves knowing that older forms might lack the specific data points required by Risk Rating 2.0. If the certificate was issued before the 2023 digital submission mandate, your agent might suggest a new survey to secure the best possible insurance rate.

What happens if my home’s lowest floor is below the Base Flood Elevation?

If your lowest floor is below the Base Flood Elevation (BFE), you'll likely face higher flood insurance premiums due to increased risk. This "negative elevation" indicates that the living space is more susceptible to water intrusion during a major storm. Additionally, being below the BFE triggers the 50% rule, meaning any major renovations could require you to physically elevate the entire structure to meet modern building codes.

Does a brand-new home automatically come with an elevation certificate?

Yes, brand-new homes in Special Flood Hazard Areas must have an elevation certificate to receive a final Certificate of Occupancy. Builders are required to provide a "finished construction" survey once the home is complete to prove compliance with local floodplain ordinances. When buying new construction, always ensure the builder provides the digital copy that was submitted to the state database as required by Florida law.

How much does an elevation certificate typically cost in Southwest Florida?

Costs for a residential elevation certificate in Southwest Florida vary based on the property's location and structural complexity. While simple residential surveys are relatively straightforward, complex luxury estates with multiple crawlspaces or unique foundations may require more intensive field work. We recommend getting quotes from at least two licensed Professional Surveyors and Mappers to ensure competitive pricing for your specific property type.

Where can I find my elevation certificate online for free in Collier County?

You can search for existing certificates through the Collier County Floodplain Management office or the Florida Division of Emergency Management (FDEM) public portal. Many certificates filed after January 1, 2023, are available digitally through these state-mandated databases. If the property is within Naples city limits, the city's dedicated flood information portal is another excellent resource for historical records and digital copies.

Is an elevation certificate required for private flood insurance in Florida?

Private flood insurance carriers in Florida don't always mandate an elevation certificate, but having one is a powerful negotiation tool. understanding Florida elevation certificates allows you to prove your home's actual height if a private company's internal mapping software overestimates your risk. Providing a certified survey can often unlock lower rates that aren't available through standard automated quoting systems used by many private insurers.

Comments