Buying a House in a Flood Zone in Bonita Springs: The 2026 Buyer’s Guide

- Team 239

- May 16

- 13 min read

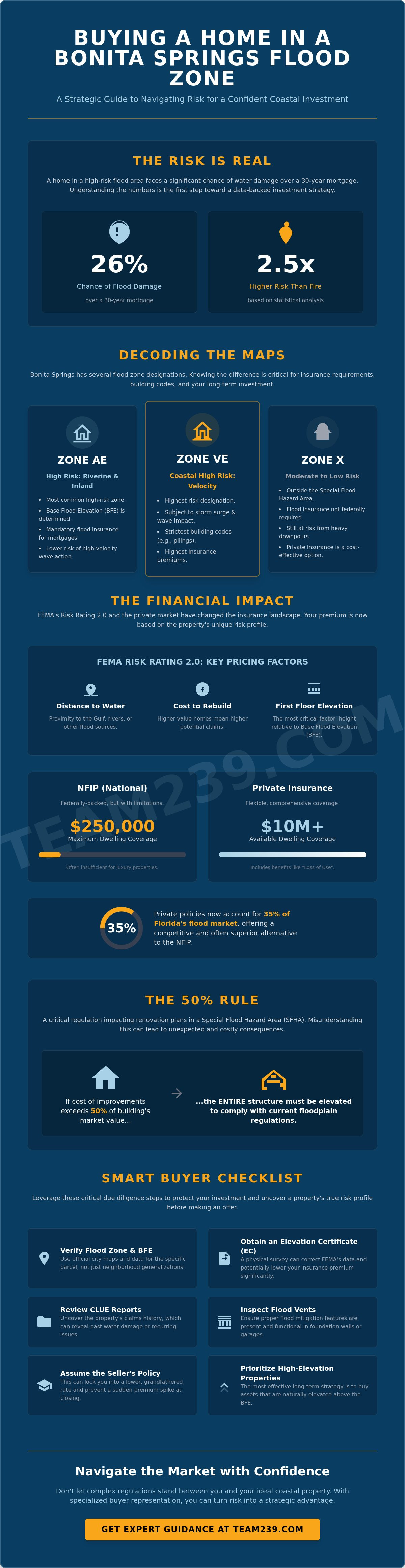

A home in a high-risk flood area has a 26% chance of suffering water damage over a 30-year mortgage, which is two-and-a-half times the statistical risk of a fire. If you are considering buying a house in a flood zone Bonita Springs, these numbers should not scare you away from a premier coastal lifestyle. Instead, they should drive a data-backed investment strategy. We recognize that deciphering FEMA maps and the 50% rule often feels like learning a new language under pressure. You want the beauty of the Gulf without the fear of uninsurable property or hidden renovation traps.

We understand that the complexity of modern regulations can make even the most experienced buyer hesitate. This guide provides the clarity you need to handle FEMA’s Risk Rating 2.0 and the targeted 2026 map updates with precision. You'll learn how the 50% rule impacts your future renovation plans, why private insurance now captures 35% of the Florida market, and how to identify high-elevation assets that protect your long-term equity. We're moving past the jargon to help you make a strategic, confident investment in the Bonita Springs market.

Key Takeaways

Decode the differences between Zone AE and VE to identify which high-risk designations require mandatory flood insurance and specific construction standards.

Understand how FEMA’s Risk Rating 2.0 calculates premiums based on individual property data rather than just map lines.

Navigate the 50% rule with confidence to ensure your renovation plans for buying a house in a flood zone Bonita Springs remain viable and compliant.

Use CLUE reports and flood vent inspections as critical due diligence steps to uncover a property's hidden history and structural mitigation.

Leverage specialized buyer representation to find high-elevation properties and obtain precise insurance quotes before making an offer.

Table of Contents

Understanding Bonita Springs Flood Zones: Maps and Terminology

Smart investing starts with data. When Understanding Bonita Springs Flood Zones, you'll first encounter the Special Flood Hazard Area (SFHA). This isn't just a technical label. It's a regulatory boundary. If you're buying a house in a flood zone Bonita Springs with a federally backed mortgage, the SFHA makes flood insurance a requirement, not an option. Lenders view these zones as areas where the annual chance of flooding is 1% or greater. It's a baseline for risk that dictates your carrying costs from day one.

Zone AE is the most common high-risk designation in our local market. It indicates a significant risk but typically lacks the intense wave action associated with the immediate coastline. As you move west of US-41 toward the Gulf, you'll likely see Zone VE. This is the coastal high-risk zone. It accounts for velocity, meaning the potential for storm surges and wave impact. Properties in VE zones often face stricter building codes and higher insurance premiums because the structural risk is fundamentally different. We prioritize identifying these nuances early in your search to avoid surprises during the inspection period.

Don't let Zone X give you a false sense of security. While FEMA labels it as minimal risk, it doesn't mean no risk. Localized street flooding or heavy tropical downpours can still impact these homes. Many savvy buyers choose private flood insurance here anyway. It's a strategic move, especially since private policies in Florida can be 20-35% cheaper than NFIP rates for moderate-risk areas. To get specific, use the City of Bonita Springs "Find My Flood Zone" app. It’s a user-centric tool that maps your specific parcel against the effective 2022 FIRM updates and the targeted 2026 revisions.

The Imperial River vs. Coastal Flood Risks

Flooding in Bonita Springs isn't a monolith. Downtown and areas near the Imperial River face riverine flooding. This happens when the river crests after heavy inland rains. It’s a different beast than the surge-based risks found west of US-41. While the coast deals with the Gulf's power, riverine zones deal with drainage basins. The city's 2026 drainage improvements have started to stabilize certain map panels, but staying informed on specific revisions is still vital for a strategic purchase.

Base Flood Elevation (BFE) Explained

Base Flood Elevation is your most important metric. It represents the height water is expected to reach during a base flood. In 2026, this is the gold standard for insurance pricing under Risk Rating 2.0. If a home’s finished floor is below BFE, expect higher costs. Bonita Springs also utilizes "Freeboard," which requires new construction or major renovations to sit even higher than the BFE. This extra layer of protection isn't just about safety; it’s a systemic approach to lowering your long-term insurance overhead.

The Financial Impact: Flood Insurance and 2026 Premiums

FEMA’s Risk Rating 2.0 has fundamentally shifted how we calculate the cost of ownership in Southwest Florida. In the past, being "in" or "out" of a zone was the primary driver of cost. Today, the National Flood Insurance Program uses a more granular methodology. It evaluates distance to water, the cost to rebuild, and the specific elevation of your first floor. Data drives the price. This means two identical houses on the same street could have different premiums. When buying a house in a flood zone Bonita Springs, you need a quote based on the specific property ID, not just a neighborhood average.

Elevation Certificates (ECs) remain a critical tool for buyers. While Risk Rating 2.0 uses proprietary software to estimate elevation, a physical EC signed by a surveyor can often correct errors in the model. If the certificate proves your home sits higher than FEMA’s data suggests, your premium could drop significantly. For homes with federally backed mortgages, flood insurance isn't optional. You can often assume the seller's existing policy. This strategy allows you to maintain their current rate "glide path" and avoid a sudden jump to full-risk pricing at closing. Our specialists often review existing policies during the due diligence period to ensure our clients aren't overpaying.

NFIP vs. Private Flood Insurance in Florida

The private insurance market has exploded. It now accounts for 35% of Florida’s flood policies as of February 2026. For luxury buyers, the NFIP’s $250,000 dwelling limit is rarely enough. Private carriers offer coverage up to $10 million or more. They include "loss of use" benefits that pay for temporary housing after a flood. These private policies also feature shorter waiting periods, typically 10 to 14 days compared to the NFIP’s 30-day requirement. Buying a house in a flood zone Bonita Springs requires a clear understanding of these private vs. public trade-offs. In moderate-risk areas like Zone X, private options often provide 20-35% savings over federal rates.

Community Rating System (CRS) Discounts

Bonita Springs is a proactive community. The city’s 2025-2026 CRS Floodplain Management Plan Annual Progress Report highlights ongoing drainage and outreach efforts that earn residents substantial discounts. Because of these municipal efforts, homeowners in the SFHA typically receive a significant reduction on their NFIP premiums. Insurance is not optional, but it can be more affordable. Always verify that your insurance agent is applying the Bonita Springs CRS credit to your policy. It’s a direct financial reward for the city's commitment to superior floodplain management and infrastructure maintenance.

The 50% Rule: Renovation Restrictions in Bonita Springs

The "Old Florida" charm of ground-level cottages often comes with a significant regulatory catch. If you're buying a house in a flood zone Bonita Springs, you must master the 50% rule. Technically known as the Substantial Improvement or Substantial Damage (SI/SD) regulation, this rule is a cornerstone of FEMA's floodplain management. It’s designed to ensure that homes in high-risk areas eventually meet modern safety standards. If the cost of your repairs, additions, or improvements equals or exceeds 50% of the building's market value, the entire structure must be brought into current compliance. In most cases, this means elevating the home to or above the current Base Flood Elevation.

Bonita Springs applies this rule over a five-year cumulative period. This prevents owners from trying to "piecemeal" a large renovation into smaller projects to bypass the threshold. To determine your available budget, the city uses a specific formula. They take the Lee County Property Appraiser's assessed value of the structure and add 20% to establish the market value. It's a transparent, data-driven calculation. If your structure is valued at $500,000, your total renovation budget for the next five years is capped at $250,000. Exceeding this by even a small margin triggers mandatory and expensive structural updates.

Impact on Luxury Remodeling Projects

Luxury buyers often encounter this hurdle when planning high-end kitchen overhauls or adding impact-resistant windows and doors. These improvements add up quickly. Bringing a non-compliant home up to 2026 codes involves more than just lifting the house; it requires modernized electrical, plumbing, and foundation systems. The cost of compliance can often rival the cost of the renovation itself. This is why many strategic investors choose to bypass older inventory. New construction homes in Bonita Springs are built to current elevation standards from day one, which exempts them from these specific renovation restrictions and protects your long-term equity.

Strategies for Buying Older Homes

You can optimize your renovation ceiling by using a private appraisal. A licensed appraiser can often determine a higher "depreciated replacement cost" for the building than the standard tax assessment. This higher valuation increases your 50% threshold, giving you more room for luxury finishes. We also advise our clients to prioritize homes that have already been substantially improved or elevated by previous owners. Buying a house in a flood zone Bonita Springs doesn't have to limit your vision. It just requires a tactical understanding of the building's value basis before you sign the contract. We help you evaluate these numbers during the initial property tour to ensure the home fits your long-term goals.

Risk Mitigation: Smart Buying Strategies for 2026

Data is your shield. While the flood zone designation tells you about the land, the CLUE report tells you about the specific structure's history. When buying a house in a flood zone Bonita Springs, you must request this Comprehensive Loss Underwriting Exchange report early. It reveals every insurance claim filed on the property over the last seven years. If a home has a history of repeated losses, it will be flagged by carriers, leading to higher premiums or limited coverage options. We use this data to separate homes with managed risks from those with chronic drainage issues.

Walkthroughs in 2026 require a technical eye. Look for flood vents in any enclosed areas like garages or crawl spaces. These specialized openings allow water to flow through the structure rather than building up hydrostatic pressure that can collapse walls. Similarly, check the elevation of mechanical equipment. Your A/C compressor, pool pumps, and water heaters should be elevated on stands above the Base Flood Elevation. If they aren't, you're looking at an immediate out-of-pocket expense to bring them into compliance and secure a favorable insurance rate. You can consult with our buyer specialists to identify these physical mitigation features during your first showing.

Don't overlook the impact of wind mitigation. While it's technically separate from flood risk, a strong wind mitigation report significantly lowers your overall homeowner's premium. In Florida's 2026 market, carriers look for secondary water resistance and hurricane-rated roof-to-wall connections. Bundling these structural strengths with a high-elevation flood profile makes your investment more attractive to both insurers and future buyers.

Elevation Certificates: Your Most Important Document

You should never buy in an AE or VE zone without a current Elevation Certificate (EC). This document identifies the Lowest Adjacent Grade (LAG), which is the lowest point of the ground touching your home. If the LAG is significantly below the BFE, the risk of water pooling against the foundation increases. In a typical Bonita Springs transaction, the seller usually provides the existing EC. If one doesn't exist or is outdated, we recommend making a new one a condition of the contract to ensure your insurance quotes are based on reality rather than estimates.

Neighborhood Due Diligence

Individual property data is only half the story. Research how the specific street performed during Hurricanes Ian and Milton. Some neighborhoods in Bonita Springs have seen massive improvements thanks to the 2025-2026 CRS Floodplain Management Plan, which includes targeted stormwater projects and improved culvert systems. Understanding these municipal upgrades helps you find "hidden gems" where the infrastructure now exceeds the old map ratings. For more context on choosing the right community, explore our Southwest Florida Lifestyle Guide to see how different areas balance coastal beauty with modern resiliency.

How Team239 Simplifies Your Bonita Springs Home Search

Buying a house in a flood zone Bonita Springs requires more than a standard real estate agent. It demands a strategic partner who understands the intersection of elevation data and market value. We specialize in identifying high-elevation "gems" that offer the coastal lifestyle you want with a risk profile that protects your capital. Our team doesn't rely on guesswork. We use current FEMA maps, 2026 targeted revisions, and property-specific data to ensure every recommendation is backed by facts. We see real estate through a lens of engineering precision and market strategy.

Transparency is our baseline. We've built a network of specialized insurance agents who provide pre-contract quotes for our clients. This means you'll know the exact carrying costs of a property before you ever commit to a purchase. We analyze the long-term ROI of homes across various FEMA zones, helping you understand how a Zone AE designation might affect your future resale value compared to a newly constructed home. Our goal is to remove the friction from the buying process, replacing confusion with clear, actionable insights.

Expert Representation for New and Resale Homes

Navigating the complexities of coastal regulations isn't a DIY project. Whether you're looking at "Old Florida" resale properties or exploring the latest developments, our representation ensures you're protected from the hidden pitfalls of the 50% rule and evolving insurance mandates. Our expertise extends across the region, from this guide to our Naples Florida Homes for Sale guide and our specialized Luxury Homes for Sale Naples FL guide. We bring a holistic view to the Southwest Florida market, ensuring your investment is sound regardless of the zip code.

Start Your Bonita Springs Search Today

Kristin and Jonathan bring over 10 years of local market experience to every transaction. We've seen the maps change and the regulations evolve; we use that history to guide your future. You can browse our curated listings today, many of which include specific elevation data to help you filter for the most resilient properties. Don't let the technicalities of buying a house in a flood zone Bonita Springs overwhelm your search. Contact us today for a personalized flood risk consultation and let's find a property that matches both your aesthetic vision and your financial goals.

Secure Your Coastal Investment with Data

Buying a house in a flood zone Bonita Springs is a strategic move that requires a balance of lifestyle desires and technical due diligence. You now have the tools to navigate FEMA’s Risk Rating 2.0, the financial constraints of the 50% rule, and the critical importance of a current Elevation Certificate. These aren't obstacles; they're data points that allow you to invest with confidence in one of Florida's most desirable coastal markets. Success in this landscape depends on moving past the jargon and focusing on structural resilience.

Our family-led team at MVP Realty Associates brings over 10 years of Southwest Florida local market experience to your search. We specialize in high-risk coastal property transactions, ensuring you have the expert representation needed to identify resilient assets. We don't just show homes. We provide the technical analysis and specialized insurance partnerships required for a modern, risk-adjusted real estate investment. Your vision of a coastal lifestyle is achievable when backed by professional expertise.

Ready to find your next high-elevation gem? Browse Bonita Springs Homes with Expert Flood Risk Analysis today. Your perfect coastal home is within reach, and we have the data to help you secure it with total confidence.

Frequently Asked Questions

Is flood insurance mandatory in Bonita Springs?

Flood insurance is mandatory if your property sits within a Special Flood Hazard Area (SFHA) and you use a federally backed mortgage. This requirement applies to high-risk designations like Zone AE and Zone VE. Even if you pay cash, we strongly recommend coverage because homes in these areas have a 26% chance of flooding during a 30-year mortgage term. It's a critical step for anyone buying a house in a flood zone Bonita Springs.

How do I find out what flood zone a house is in?

You can identify a property's designation using the City of Bonita Springs "Find My Flood Zone" tool or the FEMA Flood Map Service Center. While the current maps became effective on November 17, 2022, FEMA is performing targeted map updates throughout Lee County in 2026. We help our clients cross-reference these maps with the latest 2026 status letters to ensure they have the most accurate data before closing.

What is the difference between Zone AE and Zone X?

Zone AE is a high-risk area where lenders require flood insurance for most loans. Zone X is a moderate-to-low risk area where insurance is typically optional but still encouraged. While Zone X properties are statistically safer, they can still suffer from localized drainage issues. Private insurance for Zone X homes in Florida is often 20-35% cheaper than NFIP rates, providing an affordable way to mitigate unexpected risks.

Does a standard homeowners insurance policy cover flood damage?

No, a standard homeowners insurance policy does not cover damage from rising water or storm surges. You must secure a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private carrier. Private policies are increasingly popular in Florida, now making up 35% of the market, because they often include "loss of use" coverage that pays for temporary housing if you're displaced by a flood.

What is the 50% rule for home improvements in Florida?

The 50% rule states that if the cost of renovations or repairs equals or exceeds 50% of the building's market value, the entire structure must be brought into compliance with current flood codes. In Bonita Springs, this is tracked over a five-year cumulative period. The city calculates market value by taking the Lee County Property Appraiser's assessed value of the structure and adding 20%. This often requires elevating the home to the 2026 design flood elevation.

How much does flood insurance typically cost in Bonita Springs?

Premiums vary based on your home's specific elevation and distance to water under FEMA’s Risk Rating 2.0. For a house in Zone AE, an NFIP policy might range from $1,500 to $4,000 per year. Private policies for the same home could range from $1,200 to $5,000 depending on the carrier and coverage limits. We recommend obtaining a property-specific quote during your inspection period to avoid any surprises regarding your annual carrying costs.

Can I build a new house in a VE flood zone?

Yes, you can build in a VE zone, but it requires specialized coastal construction techniques. These homes must be elevated on pilings or columns to allow storm surges to pass underneath the living area. You cannot have permanent obstructions below the Base Flood Elevation, and all mechanical equipment must be raised. While these requirements increase initial construction costs, they significantly improve the home's resilience and can lead to lower insurance premiums over time.

What should I look for in an elevation certificate?

Focus on the Base Flood Elevation (BFE) and the height of the Lowest Finished Floor. If your floor height is at or above the BFE, your insurance rates will be more favorable. You should also check the Lowest Adjacent Grade (LAG) to see how the land slopes toward the foundation. An accurate certificate is the most important document when buying a house in a flood zone Bonita Springs, as it proves your home's actual risk level to insurers.

Comments