Flood Zone Maps for Marco Island, FL: The 2026 Homeowner’s Guide

- Team 239

- May 15

- 13 min read

On Marco Island, your home's most important document isn't your deed; it's the flood map. With high-risk premiums in Florida potentially climbing over $15,000 annually, mastering the flood zone maps for Marco Island FL is now the primary requirement for protecting your equity. You've likely felt the stress of shifting FEMA regulations and the uncertainty of how new building codes will impact your property value. It's a common concern as the local market shifts toward buyers and inventory levels rise, making every detail of a home's risk profile more critical than ever.

We're here to turn that confusion into a strategic advantage. This guide provides the clarity you need to navigate 2026 insurance requirements and secure your investment's long-term value with total confidence. We will explore the critical differences between AE and VE zones, explain how the city's CRS Class 5 rating earns you a 25% discount on premiums, and provide an actionable plan for insurance mitigation. You'll gain a professional's perspective on how to leverage these maps for better financial outcomes and a more secure future in our coastal community.

Key Takeaways

Master the latest flood zone maps for Marco Island FL to identify your property's specific risk profile and ensure compliance with 2026 insurance mandates.

Decode the technical differences between AE and VE zones to understand how wave action and elevation requirements impact your home's structural integrity and building codes.

Discover how FEMA Risk Rating 2.0 prioritizes individual property features over broad map designations, shifting the financial landscape for luxury coastal investments.

Learn to navigate the Marco Island GIS portal with a precision-focused guide to searching parcel data and interpreting interactive flood data.

Acquire strategic due diligence and marketing techniques for buying or selling high-end real estate in velocity zones to maximize property value and buyer confidence.

Table of Contents

Understanding the 2026 Flood Zone Landscape in Marco Island

Marco Island is more than just a luxury destination; it's a geographic marvel. As a barrier island, it sits on the front lines of the Gulf of Mexico. This position makes water management a core part of the local infrastructure. Understanding the flood zone maps for Marco Island FL is essential for any homeowner who wants to protect their equity in 2026. These maps aren't static documents. They represent a sophisticated blend of topographic data and climate modeling. Because the island is largely composed of dredge-and-fill land, the interaction between canal levels and storm surges is a primary focus for the latest revisions.

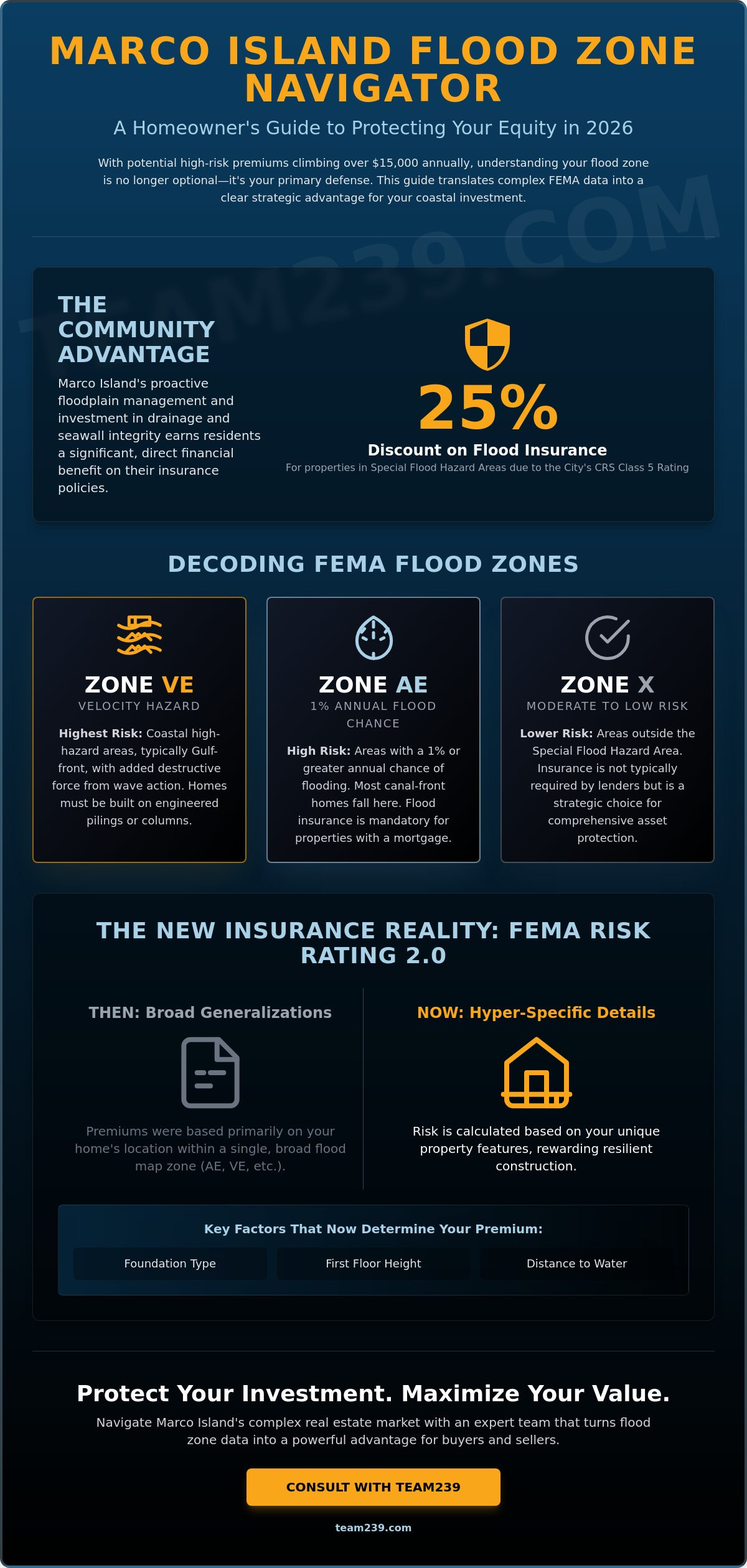

Local efforts significantly lower the cost of living here. The City of Marco Island maintains a CRS Class 5 rating. This achievement is the result of rigorous floodplain management and community outreach. Because of this rating, residents receive a 25% discount on flood insurance for properties in Special Flood Hazard Areas. This is a direct reward for the city's investment in drainage and seawall integrity. These discounts apply to policies within the National Flood Insurance Program, making high-risk zones more financially manageable for luxury property owners. Our community's proactive stance on mitigation helps stabilize property values even as federal requirements shift.

The Evolution of Marco Island Flood Mapping

FEMA map revisions in Southwest Florida have evolved from simple paper charts to digital, high-resolution models. The current FIRMs, which became effective on February 8, 2024, provide the baseline for all 2026 insurance ratings. This data is more precise because it incorporates recent storm surge data and updated elevation certificates. We've seen a transition from binary "In or Out" zones to a model that values specific home features. Risk is now calculated based on the individual property's foundation type and its exact distance from the shoreline. It's a move toward transparency that rewards homeowners who build to modern standards.

Why Homeowners Must Monitor Map Changes Regularly

Map changes can trigger immediate shifts in mortgage requirements. If your home is rezoned, your lender will likely require a policy through the National Flood Insurance Program. Grandfathering rules are more restrictive now, meaning older policies might not carry over the same benefits during a property sale. Monitoring these changes is a vital part of maintaining the Southwest Florida lifestyle you've worked hard to build. It's about staying ahead of the curve to ensure your property remains a liquid and valuable asset in an evolving market.

Decoding FEMA Designations: AE, VE, and X Zones Explained

FEMA uses specific codes to categorize risk across the island. On a landscape where water is integrated into the architecture, these codes dictate everything from foundation design to your annual carrying costs. When you examine the flood zone maps for Marco Island FL, you'll primarily see three designations: AE, VE, and X. Each one carries a different set of rules for how you build, how you insure, and how you protect your equity in the long term.

Zone AE is the most common designation you'll find on Marco Island. It represents a high-risk area with a 1% annual chance of flooding. Most canal-front homes fall into this category. While it requires mandatory flood insurance for properties with a mortgage, it doesn't carry the same extreme structural requirements as the beachfront. Zone X, divided into shaded and unshaded areas, represents the island's moderate-to-low risk zones. Insurance isn't usually a lender requirement here, but it's a strategic choice many residents make to safeguard their assets against Florida's unpredictable tropical systems.

Zone AE vs. Zone VE: Key Differences for Luxury Buyers

The distinction between AE and VE is critical for anyone looking at high-end coastal real estate. The "V" in VE stands for velocity. These are coastal high-hazard areas, typically found along the immediate Gulf front, where wave action adds kinetic force to rising waters. Because of this, VE zones require specific engineering. Homes must be built on pilings or columns to allow wave energy to pass underneath the structure. Enclosures below the flood level must use breakaway walls designed to fail under pressure without compromising the home's main supports.

Waterfront location doesn't always equate to a VE designation. Many properties on the island's extensive canal system are sheltered from direct wave action, keeping them firmly in Zone AE. This is an important detail for your budget. Insurance premiums in VE zones can be significantly higher than AE zones because the risk of structural damage is greater. If you're evaluating a property's potential, our luxury property listing services can help you analyze how these specific designations impact marketability and long-term holding costs.

Base Flood Elevation (BFE) and Freeboard Requirements

The Base Flood Elevation is the most important number on your elevation certificate. Base Flood Elevation (BFE) is the regulatory standard for the 100-year flood level. It's the benchmark FEMA uses to determine how high water is expected to rise during a major storm event. However, simply building to the BFE isn't enough in 2026. Marco Island utilizes "freeboard" requirements, which mandate that the lowest floor of a new home be elevated a specific distance above the BFE. This extra height acts as a safety buffer, providing superior protection and significantly lower insurance premiums. Investing in extra elevation isn't just a safety measure; it's a calculated financial move that pays dividends in both lower annual costs and higher resale value.

The Financial Impact: Flood Insurance and Property Values in 2026

Financial literacy in Southwest Florida real estate now requires a deep understanding of flood risk. While the flood zone maps for Marco Island FL provide the geographic boundaries, the actual cost of ownership is driven by FEMA’s Risk Rating 2.0. This methodology has shifted the focus from broad zones to individualized property features. Factors like the distance to the Gulf, the cost to rebuild, and the specific foundation type now dictate your annual expenses. For investors, this means two identical homes on the same street could have vastly different insurance profiles based on their technical specifications.

The correlation between elevation and market demand is undeniable. High-elevation properties retain their value better during market shifts, a trend we also see with luxury homes for sale in Naples FL. Lenders have become increasingly cautious in 2026. Securing a 30-year mortgage in high-risk zones requires proof of continuous coverage, and any lapse can jeopardize a deal. An Elevation Certificate (EC) has become a vital sales tool. It acts as a "financial passport" for your home, proving to both lenders and buyers that the structure is built to withstand the specific risks outlined in the current maps.

Insurance Premiums: What to Expect for a Marco Island Estate

In 2026, premium ranges reflect the high-stakes nature of coastal living. Properties in AE zones typically see annual premiums between $2,000 and $5,000, while high-velocity VE zones can easily exceed $15,000. Owners of older homes must be particularly aware of the "50% Rule." If a renovation exceeds 50% of the structure's market value, the entire building must be brought into compliance with the latest flood maps. This often requires physically elevating the home, a massive capital expense. Many luxury owners are now exploring private flood insurance. These policies can offer more competitive rates and higher coverage limits than the standard NFIP options for modern, well-engineered homes.

Resale Value and Marketability

The phrase "High and Dry" is the most powerful marketing claim in the current market. With inventory increasing to over 7,000 active listings in the metro area as of February 2026, buyers are using flood risk as a primary negotiation lever. Homes that don't meet modern elevation standards are seeing deeper discounts, often selling for closer to 93.8% of their list price. Transparency is the best strategy for sellers. Disclosing flood history and map status early builds trust and prevents deals from collapsing during the due diligence period. As part of our luxury property listing services, we analyze these risk factors to position your home as a secure, long-term asset that stands out in a crowded market.

How to Access and Interpret Marco Island Interactive Maps

Accessing raw data is the foundation of any smart real estate strategy. The digital flood zone maps for Marco Island FL provide a granular look at risk that static PDF files simply can't match. To begin your research, you should utilize the City of Marco Island’s official GIS (Geographic Information System) portal. This tool allows you to bypass generalities and look at the specific data points that affect your parcel. You can search by a standard property address or, for more precision, use the unique parcel ID found on your tax bill. This is particularly useful for vacant land or new construction projects where a mailing address might not yet be fully indexed in commercial search engines.

When you view the interactive map, pay close attention to any "LOMR" (Letter of Map Revision) markers. These are official updates issued by FEMA that modify the existing Flood Insurance Rate Map. Because the primary maps were finalized in February 2024, these revisions are critical for understanding the most current 2026 landscape. Comparing this data with historical maps can also reveal trends in how the island’s topography is being reclassified over time. This long-term view helps you anticipate future shifts in insurance requirements before they become mandatory.

Using the ArcGIS Map Tool Like a Pro

The ArcGIS portal is a professional-grade tool that requires a bit of configuration for the best results. Once the map loads, open the layer list and ensure the "Flood Zones" and "Elevation Contours" layers are active. You'll want to distinguish between the "Floodplain," which is the area subject to inundation, and the "Floodway," which is the channel reserved to discharge the base flood. If you're preparing for a meeting with a provider, most portals allow you to export a high-resolution map report. This document provides a clear visual baseline for your property's risk profile. If you need expert help interpreting how these data points affect your buying power, our residential resale representation team can provide a detailed analysis of any specific address.

Alternative Resources for Flood Data

While the city portal is excellent, cross-referencing your findings adds an extra layer of security. Collier County’s flood map service often provides additional context regarding regional drainage projects. For the absolute federal standard, the FEMA Map Service Center (MSC) remains the source of truth for official FIRMs used by lenders. If you believe the map incorrectly includes your structure in a high-risk zone, you may need to consult a specialized surveyor. They can help you apply for a LOMA (Letter of Map Amendment), which, if approved, can officially remove a building from a Special Flood Hazard Area and drastically reduce your annual insurance costs.

Strategic Real Estate Decisions: Buying and Selling in Flood Zones

Real estate on a barrier island is a game of inches. While the aesthetics of a home drive the initial interest, the technical data on the flood zone maps for Marco Island FL determines the final sale price. In 2026, due diligence must extend far beyond a standard home inspection. You need to look at the structural bones and the regulatory history of the parcel. This means verifying that any past renovations followed the 50% rule and that the current elevation certificate matches the physical reality of the site.

When the risk is too high, you have to be willing to walk away. If a property requires massive structural retrofitting to remain insurable, the long-term carrying costs might outweigh the lifestyle benefits. Our team specializes in moving to southwest florida, ensuring that your transition to the island is backed by data-driven relocation consulting. We don't just look at the floor plan; we look at the floodway. This analytical approach is what separates a standard purchase from a sound investment.

Buyer Strategies for Marco Island

Smart buyers in 2026 are shifting their focus toward properties that exceed minimum requirements. Our new construction buyer representation services prioritize homes built with modern freeboard buffers, as these structures offer the most resilient insurance profiles. Before making an offer, we recommend a deep dive into the property's history:

Review Claims History: Request a CLUE report to see the last 10 years of flood insurance claims. This reveals localized drainage issues that broad maps might miss.

Analyze Elevation Certificates: Don't wait for the lender to flag an issue. Review the EC during the inspection period to confirm the lowest habitable floor height.

Negotiate for Compliance: If a home is close to the BFE limit, use that data to negotiate credits for flood vents or other mitigation upgrades.

Seller Strategies: Maximizing Value Despite the Map

Selling a luxury property in a high-risk zone requires a proactive marketing strategy. You can't leave the buyer's insurance agent to interpret the flood zone maps for Marco Island FL on their own. Instead, provide a pre-listing elevation certificate to eliminate any "fear of the unknown." This transparency builds immediate trust with high-net-worth buyers who are looking for stability. Our luxury property listing services emphasize structural integrity by showcasing flood vents, impact-resistant features, and reinforced foundations as key selling points. Proactive disclosure of flood mitigation and elevation data can prevent deal-fallout at closing by removing the element of surprise during the buyer's financing window. By positioning your home as a fortified asset, you protect your asking price and ensure a smoother path to the closing table.

Protecting Your Marco Island Investment with Professional Precision

Protecting your investment in Southwest Florida requires more than just a beautiful view. It demands a technical understanding of how the latest flood zone maps for Marco Island FL interact with your specific property features. You've learned that elevation certificates and structural mitigation are now the primary drivers of resale value and insurance affordability. By staying ahead of FEMA revisions and leveraging the city’s mitigation discounts, you can navigate the 2026 market with absolute confidence.

We offer more than just standard representation. With over 10 years of SWFL real estate expertise and a focus on luxury waterfront transactions, we provide the strategic insight you need. We maintain direct connections to local surveyors and insurance specialists to verify every detail of your property's risk profile. Contact Team239 for a Property-Specific Flood Risk Assessment to secure your home's value today. Your coastal lifestyle is an investment worth protecting with professional precision. We look forward to helping you master these complexities and thrive in our unique island community.

Frequently Asked Questions

Is all of Marco Island in a flood zone?

Yes, every square inch of Marco Island is technically located within a flood zone because it is a barrier island. While the entire island is mapped, the specific risk level varies between Special Flood Hazard Areas and moderate-to-low risk zones. Your specific designation determines whether your lender will mandate insurance and what building codes apply to your property.

What is the difference between an AE and a VE flood zone on Marco Island?

The primary distinction is the presence of velocity wave action. Zone AE is a high-risk area subject to rising water, while Zone VE is a coastal high-hazard area where storm-driven waves add kinetic force. Because of this added threat, VE zones require more advanced engineering, such as open foundations on pilings, to allow wave energy to pass beneath the structure.

How often do flood zone maps for Marco Island change?

FEMA updates the flood zone maps for Marco Island FL periodically as new topographic data and climate models become available. The current maps became effective on February 8, 2024. While major updates happen every few years, individual parcels can see changes more frequently through Letters of Map Revision based on new surveys or community mitigation projects.

Does a home in Zone X require flood insurance?

Lenders typically don't require flood insurance for homes in Zone X because it is considered a moderate-to-low risk area. However, insurance is still highly recommended since nearly 25% of all flood claims occur outside of high-risk zones. Policies in Zone X are generally much more affordable, providing a cost-effective way to protect your equity from tropical storm surge.

What is an Elevation Certificate and why do I need one in 2026?

An Elevation Certificate is an official document that verifies your home's exact height relative to the Base Flood Elevation. In 2026, this document is essential because FEMA Risk Rating 2.0 uses your home's specific elevation to determine your insurance premium. Having a current certificate ensures you aren't overcharged based on generalized neighborhood assumptions.

How much does flood insurance cost for a typical Marco Island home?

Premiums are highly individualized and depend on your property's specific risk profile. For properties in Zone X, annual costs often range from $400 to $1,200. High-risk AE or VE zones see much higher rates, with premiums often starting at $2,000 and potentially exceeding $15,000 for older homes that don't meet modern elevation standards.

Can I build a new home in a VE zone?

You can certainly build in a VE zone, but the project must comply with the island's most rigorous structural standards. This includes elevating the living area on columns or pilings and ensuring the ground level uses breakaway walls. These designs are engineered to withstand wave action while protecting the main structure, which also helps manage long-term insurance costs.

What is the 50% rule for remodeling homes in Marco Island flood zones?

The 50% rule is a FEMA regulation stating that if the cost of improvements or repairs exceeds 50% of the building's market value, the entire structure must be brought into compliance with current flood maps. For older homes, this often means the property must be physically elevated to meet 2026 height requirements. It's a vital factor to calculate before starting any major renovation on an older estate.